In the last two articles (

here and

here), we reviewed the backtest results of 28,840 short options straddles on the Russell 2000 Index (

RUT). If you haven't read the last two articles, you may want to first read the introductory article for this series

Option Straddle Series - P&L Exits.

In this post, I am going to show the P&L results in line-chart form rather than the heat map tables I used in the last articles. The data in the charts below is only for the non-IVR filtered trades. The first set of charts shows the P&L Per Day amounts, with each chart representing the results for trades started at the same days to expiration (DTE). Here are a few key points for each chart:

- Each colored line in a chart represents a particular profit taking percentage level in terms of the credit received

- The X-axis displays the loss taking percentage level in terms of the credit received

- The Y-axis displays the average normalized percent P&L per day

- The Y-axis scale is the same for all the P&L per day charts in this article

Before we go further, I want to reiterate that these returns are the average normalized returns per day. What does this mean? Here are a few points to consider, and that I considered, when calculating these P&L numbers:

- Each data point in each of the seven P&L per day charts had different average trade durations. One data point may have had an average of 15 DIT, while another may have had an average of 60 DIT. With most of these strategy variations, there were approximately 100 trades entered for each data point in the charts below. 100 times 15 is 1500 total DIT for a strategy, while 100 times 60 yields a total of 6000 DIT. The number of DIT obviously impacts the average P&L per day.

- When a straddle is entered at 38 DTE its initial portfolio margin (PM) requirement is going to be greater than say a straddle entered at 80 DTE. The difference in margin requirement can be nearly 20% greater in this example. This initial PM number must be taken into account in order to fairly compare P&L per day values...and has been in the charts below. Using dollar amounts instead of average normalized P&L per day would not necessarily take into account the different margin requirements for the different DTE variations.

With that background information finished, let's dive into the charts...

38 DTE

|

| (click to enlarge) |

A couple of patterns stand out here. The first is that if you want to maximize your P&L per day at 38 DTE, you should take your profits at 10% and losses at 25%...diminishing returns after that loss level. That loss level also seems to be the best for the other profit taking levels at 38 DTE.

45 DTE

|

| (click to enlarge) |

At 45 DTE, you can maximize your P&L per day by sticking with the 10% profit taking level. The P&L per day numbers increase as we increase our loss taking level from 25%, to 50%, to 75%, with a peak clearly present at 75%. Taking larger losses than 75% doesn't make sense at 45 DTE.

52 DTE

|

| (click to enlarge) |

At 52 DTE, it doesn't make much sense taking a loss greater than 50%, and a case could be made to stick with a loss level of 25% to maximize your P&L per day for several variations. The 45% profit taking level was the top performer at 52 DTE. The 10% profit taking level wasn't far behind when taking losses at 25% of the credit received.

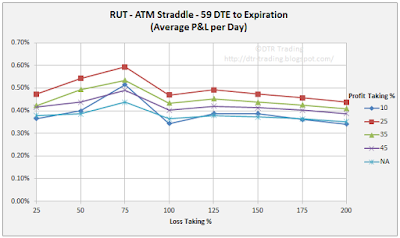

59 DTE

|

| (click to enlarge) |

At 59 DTE, the 10% profit taking level really slips behind, with the 25% and 35% profit taking levels showing the greatest P&L per day readings. The loss taking levels show a clear pattern here...as losses are increased from 25%, to 50%, to 75%, P&L per day readings increase for all of the profit taking levels. At 59 DTE, don't set your loss threshold greater than 75%...your P&L per day numbers drop off rapidly after this loss level.

66 DTE

|

| (click to enlarge) |

At 66 DTE, the 50% loss taking level has only slightly lower P&L per day readings than the 75% loss taking level for the four top performers. There is a clear trend of increasing P&L per day readings as the loss levels are increase from 25%, to 50%, to 75%. At 66 DTE, the top profit taking levels are 35% and 45%. As with the 59 DTE variations, don't set your loss level greater than 75% for the 66 DTE variations.

73 DTE

|

| (click to enlarge) |

At 73 DTE, we can maximize our P&L per day by using a 10% profit taking level and a 50% loss taking level. The maximum P&L per day value for the 25% profit taking level also occurs with a 50% loss taking level. The other profit taking variation all see a maximum P&L per day value at the 75% loss taking level.

80 DTE

|

| (click to enlarge) |

At 80 DTE the P&L per day readings for a given profit taking level do not change too much with different loss taking levels...the lines are fairly flat...except for the 10% profit taking line. For the 80 DTE variations, you might want to set your loss level at 25%, since it seems that there is not much of an increase in P&L per day if you let your losses expand beyond this point. At 80 DTE, the 25% profit taking level was the top performer.

----

The next set of charts contains the average

normalized P&L

per trade for the seven different DTE reviewed in my RUT straddle backtest series. The different initial PM requirements were used when calculating the P&L per trade numbers similar to how the PM was used in calculating the P&L per day numbers. Also, as above, the next seven charts use the same Y-axis scale...now to the charts.

38 DTE

|

| (click to enlarge) |

The greatest P&L per trade numbers were associated with the variations that carried trades to expiration (NA) rather than using a profit taking target. The greatest P&L per trade value for the 10% profit taking variations occurred at the 25% loss level. The other variations had their greatest P&L per trade values at the 100% loss level.

45 DTE

|

| (click to enlarge) |

If you choose to trade at 45 DTE, the magic loss taking level is 75%...taking a greater loss than this does not increase your P&L per trade.

52 DTE

|

| (click to enlarge) |

At 52 DTE, you pretty much hit your max P&L per trade numbers at the 50% loss taking level. P&L per trade increases as you increase the profit taking percentage from 10% to expiration (NA).

59 DTE

|

| (click to enlarge) |

At 59 DTE, there is a clear trend of increasing P&L per trade as you increase the loss taking level from 25%, to 50%, to 75%...with a drop in P&L per trade as you increase the loss taking level above this point.

66 DTE

|

| (click to enlarge) |

P&L per trade numbers are still greater at 66 DTE than at shorter DTE levels. At 66 DTE, profit taking at 45% showed the highest returns. We continue to see the trend of increasing P&L per trade as the loss taking levels are increased up to 75%. No reason to use a loss level of greater than 75%, since there are lower per trade returns after this point.

73 DTE

|

| (click to enlarge) |

At 73 DTE, the loss taking levels of NA, 45%, and 35% are clustered together, and reach a maximum P&L per trade at the 75% loss taking level. For the 25% and 10% profit taking levels, the maximum P&L per trade values occur at the 50% loss taking level.

80 DTE

|

| (click to enlarge) |

Up until this point, P&L per trade has been increasing with DTE. But at 80 DTE, the maximum returns per trade are lower for profit taking levels above 10%. Also, at 80 DTE we do not see the peak returns occur at the 75% loss taking level...the returns per trade continue increasing all the way to the 150% loss taking level...except for the 10% profit taking level. The 10% profit taking level showed maximum per trade returns at the 50% loss taking level at both 73 DTE and 80 DTE.

For most of the charts, the 10 percent profit taking level and the 25% loss almost always yielded a return of 5% on the PM requirement...and the PM requirement becomes smaller as we move out in DTE. So, 5% at 38 DTE is going to be a greater dollar amount than 5% at 80 DTE. I thought the data around the 10% profit taking level was interesting.

When we are actually trading these straddles, not just analyzing the data, we need to consider effective capital utilization. Let's look at a quick example:

- Profit taking at the 10 % level will generally have your DIT at about 30% of DTE. So, for a 38 DTE trade we can expect to be in the trade for approximately 11 days, while an 80 DTE trade would last approximately 24 days to hit the same 10% profit taking level.

- For the 10% profit taking level, using a 25% loss target, will yield approximately a 5% return on PM at both 38 DTE and 80 DTE...but the 5% number will be a larger dollar value at 38 DTE than at 80 DTE.

- This is a slightly contrived example, but it illustrates how to consider applying the data in my blog posts to your trading.

When we consider profit taking targets we need to consider how these targets impact DIT. Here are a few approximations that seem to hold with RUT straddles:

- The 10% profit taking level will have your DIT at approximately 30% of DTE

- The 25% profit taking level will have your DIT at approximately 60% of DTE

- The 35% profit taking level will have your DIT at approximately 70% of DTE

- The 45% profit taking level will have your DIT at approximately 80% of DTE

Don't forget, that as the profit taking level is increased, the win rate drops. See my

RUT Straddle Summary Page for links to all of the articles in the series. Lastly, over the next several days I will tweet (

@DTRTrading) win rate line-charts and DIT line-charts, similar to those above.

Follow my blog by email, RSS feed or Twitter (@DTRTrading). All options are available on the top of the right hand navigation column under the headings "Subscribe To RSS Feed", "Follow By Email", and "Twitter".