I've been a little curious how the SPX strangle has been performing since I last analyzed its results back in 2015 (

here). For this article, we'll just look at the following variations and how they performed from January 2007 through December 2018:

- 59 DTE - 16 Delta Short Strikes (100:50) / 2 DTE - exit if the trade has a loss of 100% of its initial credit OR if the trade has a profit of 50% of its initial credit OR at 2 DTE.

- 59 DTE - 16 Delta Short Strikes (100:50) / 29 DTE - exit if the trade has a loss of 100% of its initial credit OR if the trade has a profit of 50% of its initial credit OR at 29 DTE.

- 59 DTE - 16 Delta Short Strikes (200:50) / 2 DTE - exit if the trade has a loss of 200% of its initial credit OR if the trade has a profit of 50% of its initial credit OR at 2 DTE.

- 59 DTE - 16 Delta Short Strikes (200:50) / 29 DTE - exit if the trade has a loss of 200% of its initial credit OR if the trade has a profit of 50% of its initial credit OR at 29 DTE.

- 45 DTE - 16 Delta Short Strikes (200:50) / 2 DTE - exit if the trade has a loss of 200% of its initial credit OR if the trade has a profit of 50% of its initial credit OR at 2 DTE.

- 45 DTE - 16 Delta Short Strikes (200:50) / 22 DTE - exit if the trade has a loss of 200% of its initial credit OR if the trade has a profit of 50% of its initial credit OR at 22 DTE.

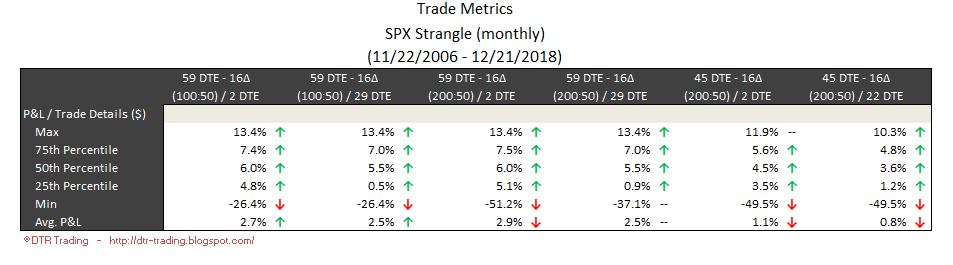

For these backtests, I used the Portfolio Margin (PM) requirements for strangles from TD/ThinkOrSwim from last weekend (13-Apr-2019). These numbers were $16K for 59 DTE strangles, and $19K for 45 DTE strangles. The performance of these variations in 2015 is shown in the tables below.

|

| (click to enlarge) |

|

| (click to enlarge) |

Now let's look at the metrics again, but adding in the results through December 2018. The tables below show the same metrics, but highlight which metrics have increased, which metrics have decreased, and which metric are unchanged.

|

| (click to enlarge) |

|

| (click to enlarge) |

The return metrics (top table) have generally improved across all variations. The variation taking losses at 100% of the credit received had improved metrics in the second table.

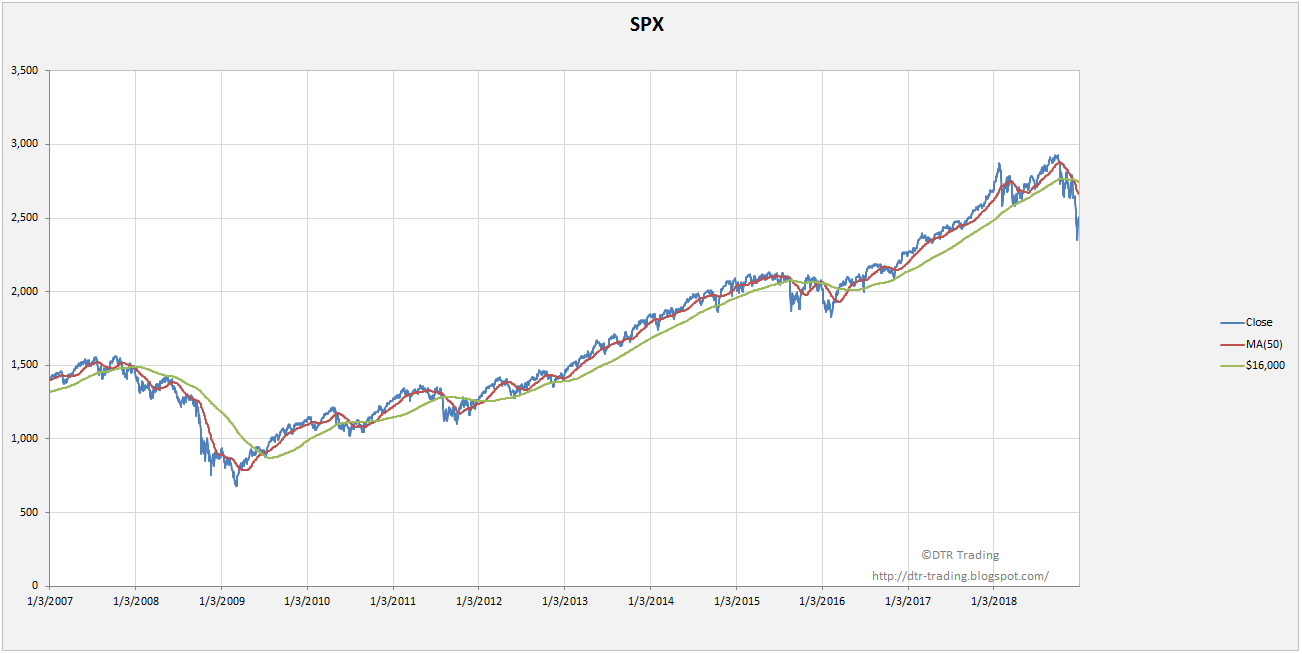

The corresponding equity curves for these variations are shown in the chart below, along with the chart of the SPX during this same time period.

|

| (click to enlarge) |

|

| (click to enlarge) |

In case you're interested, I've included the updated return percentages for each variation below.

|

| (click to enlarge) |

|

| (click to enlarge) |

|

| (click to enlarge) |

|

| (click to enlarge) |

|

| (click to enlarge) |

|

| (click to enlarge) |

If you don't want to miss my new blog posts, follow my blog either by email, RSS feed or by Twitter. All options are free, and are available on the top of the right hand navigation column under the headings "Subscribe To RSS Feed", "Follow By Email", and "Twitter". I follow blogs by RSS using Feedly, but any RSS reader will work.