- Standard: 10 put credit spreads, and 10 call credit spreads

- Delta Neutral: 10 put credit spreads, and from 5 to 10 call credit spreads - the number is adjusted at trade initiation to create a delta neutral IC. This structure will reduce losses when up moves occur during the life of the trade.

- Extra Long Put: 10 put credit spreads, 10 call credit spreads, and 1 extra long put. This structure will reduce losses when down moves occur during the life of the trade.

There are a number of approaches that we can take to dynamically exiting a trade, including:

- Price Movement Exit - for example, if the market moves past the short strike of our put spread

- Margin Loss % Exit - for example, if the loss on our position has exceeded 40% of the position margin

- Initial Credit % Loss Exit - for example, close the position for a loss if the P&L reaches 50% of the initial credit.

- Initial Credit % Profit Exit - for example, close the position for a profit if the P&L reaches 60% of the initial credit.

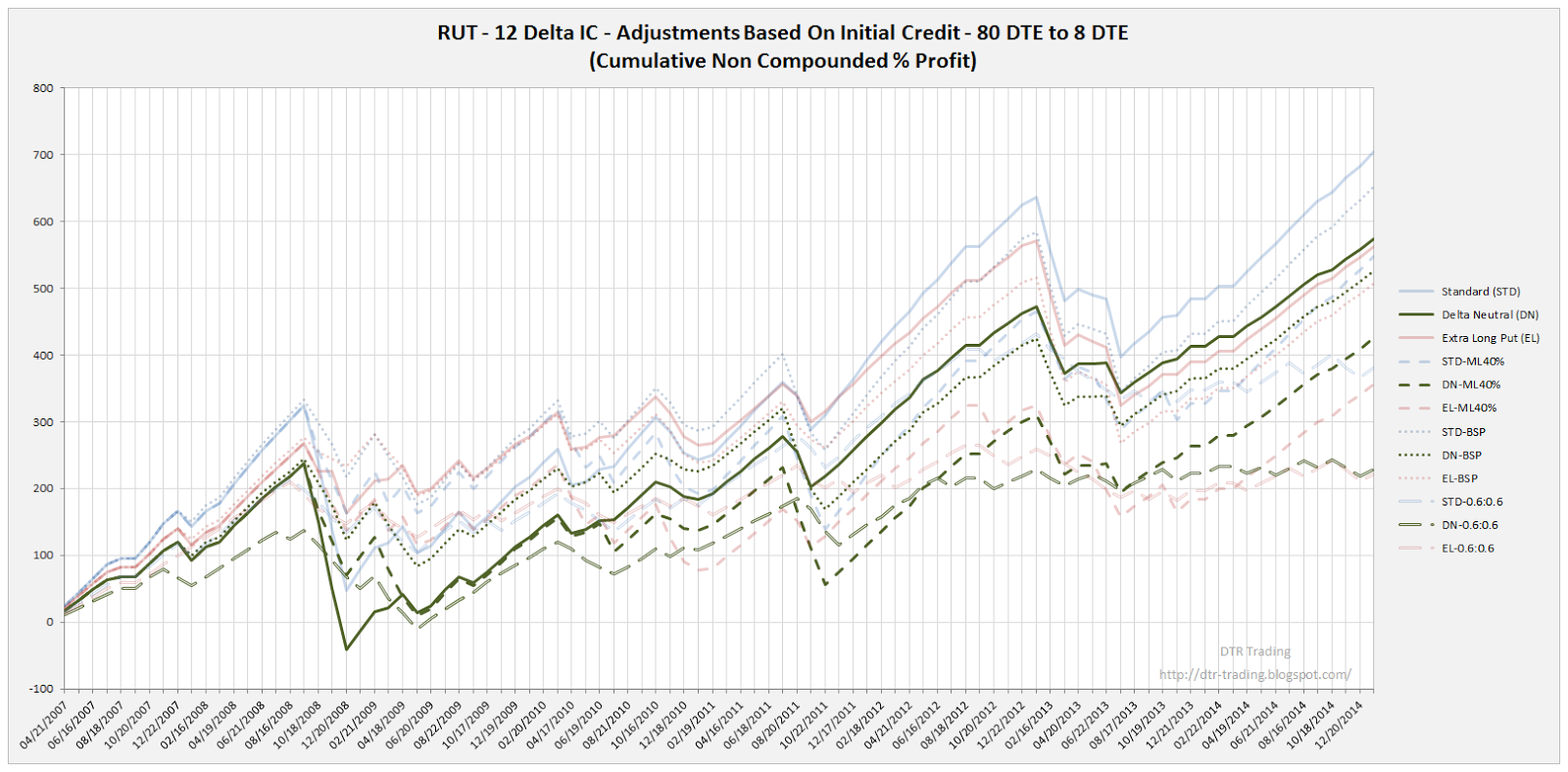

To see how these various exits perform, I have included a chart showing the equity curves (in percent terms) for the three starting structures (Standard [STD], Delta Neutral [DN], Extra Long Put [EL]) on the RUT at 66 DTE for the 12 delta short variation.

|

| (click to enlarge) |

This equity curve chart should look very similar to the equity curves in my prior posts, except for the fact that this chart is in percent rather than dollars. In the chart above, all of the STD IC versions have blue equity curves, all of the DN IC versions have green equity curves, and all of the EL IC versions have red equity curves. The solid lines represent the equity curves for the "no touch" version, while the dashed lines represent the equity curves for the dynamically exited versions.

There are three different exit versions shown in the chart above:

- ML40% - this is a Margin Loss % Exit. Trades using this exit strategy either exit at 8 DTE OR if the trade has a loss greater than 40% of the margin requirement for the trade. (ML40% = Max Loss 40%)

- BSP - this is a Price Movement Exit. Trades using this exit strategy either exit at 8 DTE OR if the price of the underlying (RUT) moves below the strike of the short put. (BSP = Below Short Put).

- 0.6:0.6 - This is an Initial Credit % Profit/Loss Exit. Trades using this exit strategy either exit at 8 DTE OR if the trade has a profit of 60% of its initial credit OR if the trade has a loss of 60% of its initial credit.

In the chart below, I've highlighted just the Standard IC (STD) versions. The SML40% exit version had the greatest profit of the STD strategies backtested, followed by the BSP exit, the STD version without dynamic stops, and finally the 0.6:0.6 exit. Recall that for the 80 DTE strategies, the order was STD version without dynamic stops, BSP exit, ML40% exit, and 0.6:0.6 exit.

|

| (click to enlarge) |

In the next chart, I have highlighted just the Delta Neutral IC (DN) versions. The SML40% exit version had the greatest profit of the DN strategies backtested, followed by the BSP exit, the DN version without dynamic stops, and finally the 0.6:0.6 exit....the same pattern we noticed in the STD strategies at 66 DTE.

|

| (click to enlarge) |

In this last chart, I have highlighted just the Extra Long Put IC (EL) versions. The SML40% exit version had the greatest profit of the EL strategies backtested, followed by the BSP exit, the EL version without dynamic stops, and finally the 0.6:0.6 exit...the same pattern we noticed in the STD and DN 66 DTE strategies.

|

| (click to enlarge) |

There are at least two points to note in the above charts. The first is that the three best performing strategies were versions of the STD strategy. The second, is that the percentages have not been normalized...the margin requirement for every trade is different. Therefore the denominator is different for every percent return. If we normalize the percentages using the maximum margin required for all 1140 trades represented in the above equity curves....which happens to be $17,760...we get the normalized equity curve chart below. This chart does not look too different from the non-normalized chart.

|

| (click to enlarge) |

If you don't want to miss my new blog posts, follow my blog either by email or by RSS feed. Both options are free, and are available on the top of the right hand navigation column under the headings "Follow By Email" and "Subscribe To RSS Feed". I follow blogs by RSS using Feedly, but any RSS reader will work.