The charts below are organized similar to those in the prior post. Each group of charts corresponds to the short delta listed in the heading bullet (8 delta, 12 delta, 16 delta, 20 delta). Each column corresponds to an IC wing width (column 1 = 25 points, column 2 = 50 points, column 3 = 75 points).

The first row in each group displays the backtest results associated with weekly data, and the second row in each group displays the backtest results associated with monthly expiration data. Weekly data could result in a new trade being initiated every week (if the entry criteria were satisfied), while the monthly expiration data would result in at most one trade per month (if the entry criteria were satisfied). The monthly data does represent a subset of the weekly data, but will more closely match actual trade results for traders who initiate on monthly expirations rather than weekly expirations.

Lastly, trades can overlap...which means there can be multiple trades active at any point in the backtesting. Opening a new trade does not require the prior trade to be closed.

In this post, we'll only review three metrics:

- Normalized P&L per day

- Normalized P&L per trade

- Win rate

Normalized P&L per Day

- 8 delta short strikes (weekly data top, monthly data bottom)

- At 8 delta, the monthly trades show a bit better P&L per day numbers than the weekly trades.

|

| (click to enlarge) |

- 12 delta short strikes (weekly data top, monthly data bottom)

- At 12 delta, the monthly trades again show better P&L per day readings than the weekly trades. The P&L lines are also more tightly grouped by profit taking level (50, 75, NA) as wing width increases, indicating that profit taking level has a larger impact on P&L per day than IC structure at this delta. We noticed this same pattern with the 38 DTE ICs.

|

| (click to enlarge) |

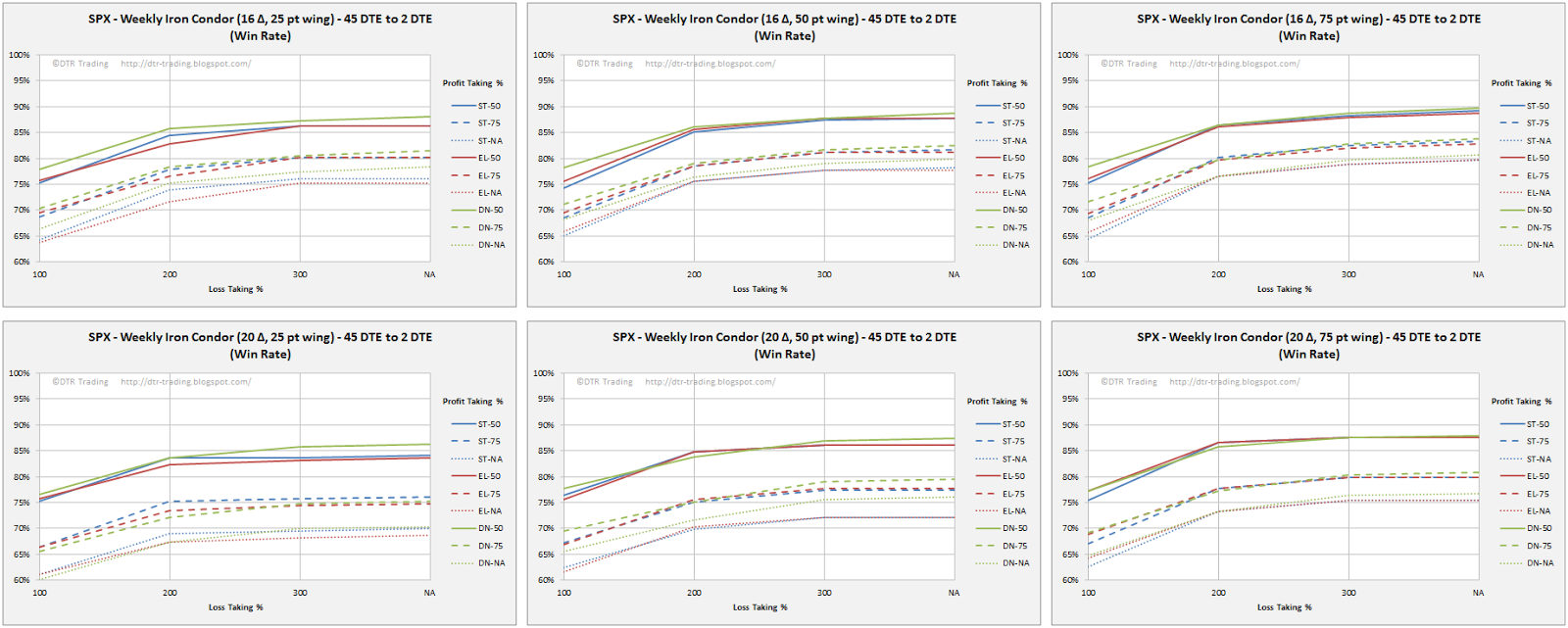

- 16 delta short strikes (weekly data top, monthly data bottom)

- The monthly trades continue to exhibit greater P&L per day readings than the weekly trades. As wing width increases, the P&L per day lines become closer to each other and appear to converge. The 50% profit taking level outperforms the other levels, and this trend is particularly strong in the monthly trade data. We also continue to see stronger clustering by profit taking level, with IC structure having a smaller impact.

|

| (click to enlarge) |

- 20 delta short strikes (weekly data top, monthly data bottom)

- At 20 delta, the returns associated with the 50% profit taking level generally outperform the other profit taking levels. We noticed this trend with the 38 DTE ICs also.

|

| (click to enlarge) |

In general, the monthly trades have higher P&L per day readings than the weekly trades, but the weekly trades typically have tighter grouping of their P&L per day lines. Another trend to note is the general slope of these P&L per day lines at 45 DTE versus 38 DTE. At 38 DTE, most of the P&L per day lines sloped down, while at 45 DTE the P&L per day lines are starting to slope up...greater P&L per day as the loss level increases. We'll need to see if this trend continues as DTE increase.

Normalized P&L per Trade

- 8 delta short strikes (weekly data top, monthly data bottom)

- In the monthly data, we see that taking the trades to expiration resulted in larger P&L per trade results than either the 50% or 75% profit taking levels..similar to the 38 DTE trades. The weekly data, shows a similar pattern, but the P&L per trade lines are more tightly grouped. Lastly, the monthly P&L per trades values are slightly greater than the weekly P&L per trade values.

|

| (click to enlarge) |

- 12 delta short strikes (weekly data top, monthly data bottom)

- Not a large difference between the monthly and weekly data for the 12 delta short strikes. The monthly data has slight out-performance with no profit taking target (ST-NA) with the 50 and 75 point wing widths

|

| (click to enlarge) |

- 16 delta short strikes (weekly data top, monthly data bottom)

- Similar to the 38 DTE ICs, as the wing widths increase, we see convergence of the P&L lines by profit taking level. As wing width increases, the IC structures have less of an impact on returns than the profit taking level.

|

| (click to enlarge) |

- 20 delta short strikes (weekly data top, monthly data bottom)

- In the weekly data, there is very little difference between the 50% and 75% profit taking levels, particularly with wing widths of 50 points and 75 points.

|

| (click to enlarge) |

There are two clear trends in the P&L per trade values:

- As wing width increases, the difference between the P&L per trade values for the different profit taking levels and IC structures decreases...the lines become more tightly grouped.

- In general, as loss taking levels increase, P&L per trade increases with the 45 DTE ICs.

- The P&L per trade values are slightly greater in the monthly trades than the weekly trades...this is likely a function of more data being available for the weekly trades, which smooths out the extreme positive and negative values

Win Rate

- 8 delta short strikes (weekly data top, monthly data bottom)

- As with the 38 DTE ICs, the 50% profit taking level outperforms the other profit taking levels at 8 delta. The win rate lines are grouped more by profit taking level than by IC structure type. The delta neutral (DN) structure out-performs the other structures at the 50% profit taking level.

|

| (click to enlarge) |

- 12 delta short strikes (weekly data top, monthly data bottom)

- At 12 delta, the 50% profit taking level continues to outperform the other profit taking levels. Win rate differences due to structure are less significant.

|

| (click to enlarge) |

- 16 delta short strikes (weekly data top, monthly data bottom)

- At 16 delta, win rate grouping by profit taking level is even more pronounced. The monthly results are also slightly better than the weekly results.

|

| (click to enlarge) |

- 20 delta short strikes (weekly data top, monthly data bottom)

- As with the 38 DTE ICs, at 20 delta, the win rate grouping by profit taking level is even stronger.

|

| (click to enlarge) |

Similar to the 38 DTE ICs, the win rate lines have a steeper slope from the 100% loss taking level to the 200% loss taking level. The slope tapers off after the 200% loss taking level. Also, as short strike deltas increase, win rate decreases.

Here are a few of the "take-aways" from the 45 DTE IC backtest results...some are duplicates of the 38 DTE "take-aways":

- Unlike the 38 DTE ICs, the P&L per trade numbers do not decrease when we move from the 100% loss taking level to the 200% loss taking level. With the 45 DTE ICs, the P&L per trade numbers increase as we increase the loss taking %. This is more pronounced at lower deltas and larger wing widths.

- As short strike deltas increase, the 50% profit taking level yields greater P&L per day numbers:

- The standard IC (ST) has better P&L per day at loss taking levels of 100% and 200%

- The delta neutral IC (DN) has better P&L per day at loss taking levels of 300% or more

- As short strike deltas increase, take profits at lower profit taking levels.

- At 8 delta, the 75% profit taking level yields greater P&L per trade numbers

- At 20 delta, the 50% profit taking level yields greater P&L per trade numbers

- The extra long put structure (EL) generally under performs the delta neutral (DN) and standard balanced (ST) structures.

- At the 50% profit taking level you will generally be out of your trade for a profit between 16 and 26 days. If you haven't hit your profit target in 26 days, you should consider closing your trade.

- The 50% profit taking level has a higher win rate than the other profit taking levels

- The 100% loss taking level generally has a lower win rate than the larger loss taking levels.

Follow my blog by email, RSS feed or Twitter (@DTRTrading). All options are available on the top of the right hand navigation column under the headings "Subscribe To RSS Feed", "Follow By Email", and "Twitter".