For background on the setup for the backtests, as well as the nomenclature used in the charts and tables below, please see the introductory article for this series: Option Straddle Series - P&L Exits.

No IV Rank Filter

In this section we will look at the results of entering one trade for every monthly expiration regardless of the implied volatility rank (IVR) of the SPX on the date of entry. Entering these trades at 45 DTE and utilizing our loss exits and 25% credit exits (described here), resulted in the equity curves below.

|

| (click to enlarge) |

The trade metrics for these different exits are shown in the table below. The (125:25) and (150:25) variations stand out with the top P&L % / day readings, highest overall P&L % values, and the highest win rate. These also happen to be the variations highlighted by Tastytrade.

|

| (click to enlarge) |

The table below shows the distribution of returns in five-number summary format. Hat-tip to Tastytrade.

|

| (click to enlarge) |

Below are three sets of scatter plots for selling 45 DTE ATM SPX straddles. The first image contains one scatter plot per strategy and shows P&L in percentage terms versus IVR for the SPX. The IVR was captured on the day each trade was initiated. The trend of increasing P&L with increasing IVR continues.

| (click to enlarge) |

The next image shows P&L in percentage terms versus initial ATM IV. This ATM IV was captured on the day each trade was initiated. Higher IV resulted in higher returns, but the majority of the profitable trades occurred at an IV below 35. It is also interesting to note that at the higher loss management levels (100 - 200) there is a cluster of losing trades in the IV range of 12 to 22...those particular losers should be investigated a bit further.

|

| (click to enlarge) |

The third image shows P&L in percentage terms versus days-in-trade (DIT). We see the same two patterns that we observed before...when managing losses early (25%, 50%), the losses were fairly evenly distributed across DIT. As the loss management becomes less aggressive (125% and higher), we see that the losses are concentrated above 25 DIT. Also, most of these losses were not realized until expiration...meaning many of these particular losses were less than our threshold values.

|

| (click to enlarge) |

IV Rank > 50% Filter

In this section we will look at the results of entering one trade for every monthly expiration only when the IVR of the SPX is greater than 50% ( >50% ). Entering these trades at 45 DTE and utilizing our loss exits and 25% credit exits (described here) resulted in the equity curves below.

|

| (click to enlarge) |

The trade metrics for these different exits are shown in the table below. There are significantly fewer trades that meet the >50% IVR criteria...roughly 20% of the available trades...this is a consistent trend with the > 50% IVR filter. The top four variations that meet this IVR criteria have high P&L% per day readings, and win rates of 86%.

|

| (click to enlarge) |

The table below shows the distribution of returns in five-number summary format.

|

| (click to enlarge) |

IV Rank < 50% Filter

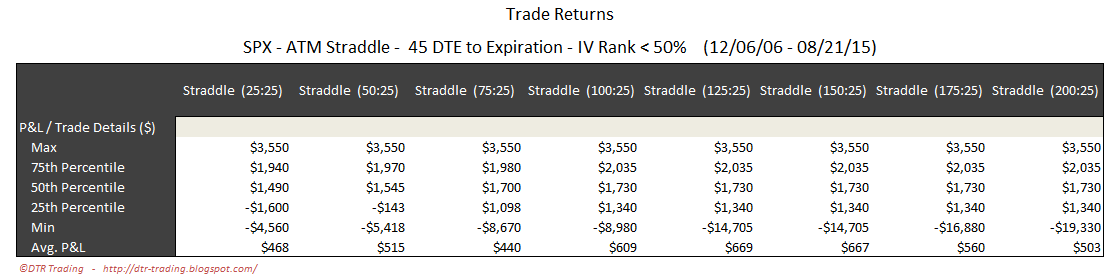

In this section we will look at the results of entering one trade for every monthly expiration only when the IVR of the SPX is less than 50% ( <50% ). Entering these trades at 45 DTE and utilizing our loss exits and 25% credit exits (described here) resulted in the equity curves below.

|

| (click to enlarge) |

The trade metrics for these different exits are shown in the table below. Using the lower IVR filter did not improve any of the metrics over the IVR > 50% filtered other than the total P&L %.

|

| (click to enlarge) |

The table below shows the distribution of returns in five-number summary format.

|

| (click to enlarge) |

In the next post we will look at the backtest results of 45 DTE ATM SPX short straddles using the same loss thresholds as above, but with profit taking occurring at 35% of the credit received.

Follow my blog by email, RSS feed or Twitter (@DTRTrading). All options are available on the top of the right hand navigation column under the headings "Subscribe To RSS Feed", "Follow By Email", and "Twitter".

5 comments:

This is much higher quality research than what is put out by TT. It is much appreciated.

Is your DIT calendar days or trading days? Also did you use the the same closing of trade at 8 DTE that you did in the IC studies?

Hi Iyad,

Thank you for the compliment...I appreciate it!

I do think TT do great work and have made profitable approaches to options trading more accessible to investors...so, I'm a fan of what they do. They have the challenge of balancing depth of research with broader audience appeal...something I don't have to contend with. Hopefully people see my work and the work of TT as complimentary.

Regarding trade closure, with my strangle and straddle research, I closed trades at expiration or at the strategy variation's profit or loss exit levels.

Thanks again,

Dave

Just realized I didn't answer your other question. Both DIT and DTE are calendar days, not trading/business days.

Would you have a updated graph for this by any chance ?

Not right now, but will probably run/publish some tests in April.

Thanks,

Dave

Post a Comment